If you’re near retirement, you may be looking forward to the day when taxes get simpler. You could be disappointed.

“The tax return changes drastically when you go from a working mode to a retired mode,” says Ed Phelps, an IRA expert from Miami.

Of course, everyone’s tax situation is different, but here are some tax issues you may encounter and ways to lessen their impact.

Deductions may disappear

If your children are grown and your house is paid off, you’ll no longer get tax breaks for dependents or mortgage interest. And you’ll no longer be able to get a tax break for contributing to a 401(k) or IRA.

Your deductions for charitable contributions may decline, too, as many retirees tend to volunteer more than donate. And starting with the 2017 tax year, taxpayers age 65 and older will be able to deduct only the amount of medical expenses exceeding 10 percent of adjusted gross income, up from 7.5 percent.

Solution: Take advantage of available tax breaks while you still can. Bunch up any elective medical expenses into one year to meet the higher health deduction. “Your last year of working, try to contribute as much as you can to your retirement plan,” says Phelps.

You may end up in a higher tax bracket

Many retirees drop into a lower tax bracket when they stop working. But after age 701/2, they must start taking minimum distributions annually from tax-deferred accounts such as a 401(k) or traditional IRA.

These distributions — on top of other income — can push retirees into a higher bracket. For example, singles with taxable income of up to $37,950 — or couples filing jointly with $75,900 — are in the 15 percent tax bracket this year. Throw in several thousand dollars from a required distribution, and that extra income will be taxed at 25 percent.

Solution: Consider taking distributions from tax-deferred accounts while still in your 60s and in a lower tax bracket, experts say. With care, you can steadily withdraw money and stay within your current tax bracket. Or convert some tax-deferred dollars into a Roth IRA. You’ll owe income taxes on the amount converted, but thereafter Roth withdrawals are tax-free. And Roths don’t have required distributions.

AARP

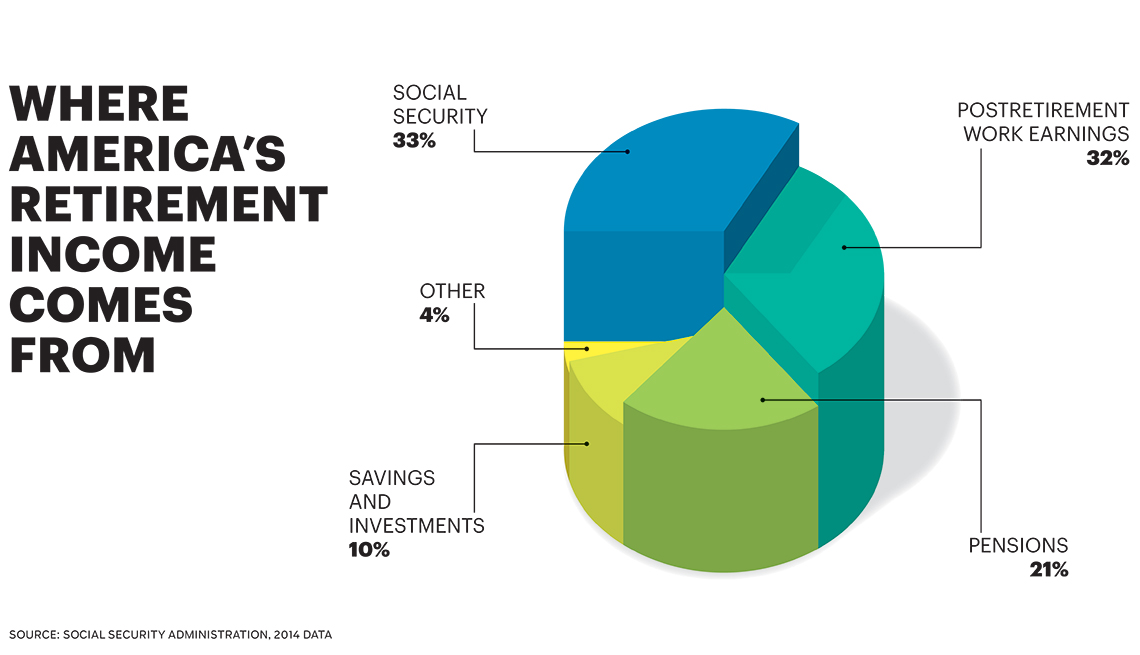

America’s retirement income is mostly from Social Security.

Your Social Security may be taxed

Many retirees are surprised to find that their Social Security benefits are taxable if their income is above a certain level. And it doesn’t take much income to trigger the tax.

Under the IRS formula, half of Social Security benefits are added to other income retirees receive. If the amount exceeds $25,000 for singles or $32,000 for married couples filing jointly, a portion of the benefits will be taxed.

Solution: Tapping tax-deferred accounts earlier in retirement will reduce future required distributions, and may provide the money to live on so you can postpone taking Social Security benefits. For every year up to age 70 that you postpone benefits beyond your normal retirement age (66 to 67 for most people), your benefits will increase 8 percent.

You may pay taxes quarterly

Your employer withholds taxes from your paycheck and forwards the money to Uncle Sam. That’s not the case in retirement, so you may have to pay estimated taxes quarterly or you may face a penalty.

Solution: You may be able to avoid quarterly payments by asking your brokerage or former employer to deduct taxes for you from your IRA withdrawals or pension check, she says. Make sure the withholding is enough to cover your tax liability.

Your finances may get more complicated

If you’ve been a good saver, you likely accumulated multiple accounts and need to withdraw that money in the most tax-efficient way.

Solution: Make this job easier for yourself by consolidating accounts. And just before retirement or during the first year, see a tax professional for advice.